Corporate ESG Performance, Cost of Debt Financing and Environmental Investments

Weiling Zhan1, Peijin Yan1*, Xinyi Wang1, Huixia Cai1

1School of Economics, Guangzhou College of Commerce, Guangzhou, Guangdong Province, China

*Correspondence to: Peijin Yan, School of Economics, Guangzhou College of Commerce, 222 Kowloon Avenue, Longhu Street, Guangzhou, Guangdong Province, 511363, China; Email: 1697021476@qq.com

DOI: 10.53964/mem.2025002

Abstract

Objective: This study examines the relationship between corporate ESG performance, environmental protection investment (EPI), and debt financing cost.

Methods: Using empirical data from Chinese A-share listed companies between 2008 and 2022, construct a two-way fixed-effects model to explore the impact of corporate ESG performance on EPI, with a particular focus on the mediating role of debt financing costs.

Results: Corporate ESG performance significantly enhances EPI. In other words, strong ESG performance not only reflects corporate social responsibility but also acts as a driving force for promoting environmental investment and achieving green development. The lower the cost of debt financing, the more pronounced the positive effect of ESG performance on EPI. This suggests that superior ESG performance can reduce debt financing costs, thereby incentivizing enterprises to allocate more resources to environmental initiatives.

Conclusion: Based on these findings, this paper proposes that enterprises enhance their ESG performance by improving corporate governance, strengthening environmental awareness, and actively engaging in environmental protection projects. Additionally, it recommends that investors incorporate ESG performance into their decision-making processes and encourages enterprises to continuously improve their environmental practices.

Keywords: corporate ESG performance; corporate environmental investment; cost of debt financing

1 INTRODUCTION

Corporate ESG performance mainly involves the company's practices and performance in the areas of Environment, Social and Governance, which has become a standard for evaluating a company's ability to sustain development and an important indicator of social responsibility, and has a significant impact on the company's long-term value creation and risk management. Good ESG performance not only reflects a company's achievements in environmental protection, fulfillment of social responsibilities, and corporate management, but is also a key factor in attracting investors, improving market reputation, and reducing operational risks. Since 2009, the number of listed companies issuing ESG reports has grown from 371 to 2,124 in 2024, an increase of about 5.7 times, especially since 2021, when the growth rate has remained high according to the report: Rising Tide: An Overview of China A-Share ESG Performance 2024.

Enterprises' protective investment in the environment has gradually become a key strategy to drive their long-term development. By investing in environmental protection, companies can effectively reduce potential environmental risks, minimize operational costs, and gain a competitive advantage in the marketplace. Corporate environmental protection investment (EPI) plays an important role at multiple levels. First, direct investment in pollution control and ecological restoration projects helps reduce pollutant emissions and improve environmental elements such as water quality, air quality and soil; second, by investing in renewable energy and energy-saving technologies, it can optimize the energy structure and industrial layout and achieve win-win results for economic growth and environmental protection; third, EPI not only spawns the environmental protection technology development and application process, it also spawns the growth of environmental protection industry and promotes the transformation of traditional industries in the direction of green and low-carbon.

When promoting EPI projects, companies often face the problems of insufficient funds and poor long-term investment returns. In order to cope with these challenges, companies may choose to seek more financial support through debt financing, which will help advance environmental protection projects faster. The high outlay of debt financing has the potential to aggravate the economic pressure and increase the economic risk of the company, a situation that may inversely affect corporate investment in environmental protection. Whether studying corporate ESG performance can reduce financing costs and further motivate companies to reach higher levels of environmental investment is a topic of great interest in the environmental field.

ESG is a growing area of research. At the micro level of enterprises, existing empirical studies mainly focus on whether corporate ESG performance can create value for enterprises, such as Alareeni et al[1] studied the impact of corporate ESG performance on corporate financial performance. Existing literature mainly explores the ways in which corporate ESG performance creates value for firms in several ways, including reducing financing costs[2,3], enhancing customer satisfaction[4], and so on. Financing constraints are common mechanism variables in empirical studies of corporate green investment[5,6]. Regarding the impact of environmental investment, the existing literature focuses on external factors such as environmental regulations[7,8], but ignores corporate ESG performance. Therefore, despite the abundance of existing research, less literature has explored the impact of firms' ESG performance on environmental investments and the role that debt financing costs play in this relationship.

In summary, this paper introduces the cost of debt financing as an influential mechanism to study the impact of firms' ESG performance on firms' environmental investments. Specifically, this paper adopts a combination of theoretical and empirical empirical analysis methods, takes Chinese listed companies from 2008 to 2022 as the research samples, constructs a two-way fixed effect model to explore the impact of corporate ESG performance on corporate green investment, and further investigates the impact path of corporate ESG performance on green investment from the perspective of the cost of financing. Compared with existing studies, this paper puts corporate ESG performance, environmental investment and debt financing cost under the same framework for research, verifies the causal relationship among the three, and is conducive to enriching relevant research results. In addition, this study provides a reference basis for enterprises to actively display their ESG strategies, publicize relevant data, and take on more ESG responsibilities in environmental protection, social responsibility and corporate management, which is conducive to improving the effectiveness of their actions and practical performance in the ESG field and promoting enterprises towards sustainable development.

2 MATERIALS AND METHODS

2.1 Theoretical Analysis and Hypothesis

2.1.1 Theoretical Basis

2.1.1.1 Theory of Social Responsibility

The theory of Corporate Social Responsibility recognizes that while pursuing economic returns, a company must also consider the impact it may have on its employees, customers, communities, the environment, and all those who have an interest in its well-being, so as to proactively assume its social responsibility. This notion is closely linked to sustained corporate growth, innovative thinking and values, and has gradually been transformed into a core topic of general interest in both academia and practice. The view represented by Porter et al[9] is that corporate social responsibility is not only conducive to obtaining social support and competitive advantage, but also urges innovative activities. As society demands more and more from companies to be socially responsible, companies that actively fulfill their social responsibility have an early strategic advantage, which in turn ensures their long-term economic performance. When a company demonstrates excellence in social responsibility, it not only enhances the impact of its brand and improves its competitive position in the marketplace, it may also reduce the overall cost of debt financing. At the same time, by investing in environmental protection, a company not only helps to alleviate the negative impact of environmental issues, but also enhances the efficiency of resource utilization, which in turn promotes the long-term sustainable development of the company.

2.1.1.2 Signaling Theory

There is an information asymmetry in the ESG field, which is mainly reflected in the fact that there is a certain lack of practical knowledge of corporate ESG among investors and other relevant interest groups. External investors in listed companies have an unavoidable shortcoming in terms of data availability when compared to internal business managers. This situation leads to a constant disadvantage for outside investors as different information holders will convey different information to stakeholders. Signal Theory[10] is considered in economics as an academic model used to explain how one participant communicates information to the other through specific signals in the context of information asymmetry. Based on this theory, corporations should improve the transparency and truthfulness of ESG information to reduce investment costs and promote EPIs.

A company's ESG performance can often serve as a signal that it is placing a high priority on sustainable development and environmental protection, and such an initiative may be able to strengthen external stakeholders' trust in the company's long-term effectiveness. At the same time, good ESG performance can be seen as a sign that a company is communicating its inherent values and long-term vision to the outside world. The public release of ESG information by a firm can effectively reduce the imbalance of information with the outside world and increase its transparency, thereby strengthening trust with investors and enhancing its brand image, as well as lowering investors' predictions of its potential risks. From the perspective of a company's cost of debt financing, a company's good ESG performance usually reflects a sign that its business operations are stable and its risks are relatively low. Such signals can attenuate creditors' predictions of a firm's possible default risk, which in turn may trigger a reduction in the cost of debt financing. In short, firms that exhibit ESG may be recognized as more trustworthy and less risky investment targets, and in turn raise capital at lower fees. Signaling theory provides a theoretical basis for understanding and improving firms' ESG performance, emphasizing the role of disclosure in promoting environmental investment and reducing financing costs.

2.1.2 Hypothesis

2.1.2.1 The Impact of ESG Performance on Environmental Investments

ESG has become an important indicator of corporate sustainability and social responsibility, and has a significant impact on a company's ability to attract consumers.The performance of ESG companies may, to some extent, have a profound effect on their overall reputation and brand value. And as consumers gradually become more aware of environmental issues, companies that are able to excel in ESG tend to have the potential to build even better brand images and reputations[4]. When consumers choose to purchase environmentally friendly products and sponsor environmentally friendly companies, a company's performance in this area can directly affect its performance and competitiveness in the marketplace. In addition, good ESG performance does not only lead to more recognition and social acclaim in the marketplace, but also to numerous business opportunities for the company and broad support from other stakeholders. On the basis of good economic performance and stakeholder support, companies have the strength and energy to carry out environmental investment projects with high risks and long return cycles. Therefore, the better a company's ESG performance, the better its economic performance, thus providing stronger support for EPI. Enterprises that do not perform satisfactorily in environmental protection may encounter various risks such as lawsuits and environmental accidents, all of which may negatively affect the long-term development and value of the enterprise. With this negative impact, the progress of the firm's green investment program will also likely come to a standstill.

Since external investors usually do not have access to the same level of environmental information as within the enterprise, they may be limited in making investment decisions, resulting in high financing costs for the enterprise, which is not conducive to the enterprise's environmental investment. In order to reduce this information asymmetry, it is crucial to improve the transparency of environmental information. By enhancing corporate EGS performance, listed companies demonstrate to their investors a strong commitment to environmental protection and the possibility of sustainable development, which will help investors to obtain more accurate, truthful and comprehensive environmental information, and thus make a more informed assessment of and response to corporate ESG performance. Corporate ESG performance can reduce the opacity of information, and companies with excellent ESG performance can bring more lasting value to the company, which can attract many investors as well as capital injection and drive corporate EPI. In addition, after evaluating and considering ESG factors, investors are more likely to screen and support enterprises and projects with strong environmental awareness and sense of responsibility, so as to promote the prosperity of the environmental protection industry, reduce the risk to the environment, enhance the long-term value of the enterprise and brand image, and motivate enterprises to carry out more EPI behavior.

Based on the previous analysis, this paper proposes the following research hypothesis H1: The better the ESG performance, the higher the level of corporate environmental investment.

2.1.2.2 ESG Performance, Corporate Environmental Investment and Debt Financing Costs

The theory of information asymmetry states that the information gap between the demander and the provider of funds deepens the difficulty and pushes up the cost of financing. Among the many companies seeking financing, those with less information asymmetry are more likely to be favored by banks and other financial institutions, and may be able to obtain more loans or more favorable interest rates.The provision of ESG information can effectively reduce information asymmetry and have a positive impact on financing activities. A company that excels in ESG can effectively reduce the information imbalance between creditors and debtors, thereby accurately assessing the company's ability to repay its debts and improving its credit rating. This not only makes it easier for the company to raise capital, but also mitigates risk premiums and transaction costs, which in turn reduces financing costs. In addition, excellent ESG performance helps to increase investors' interest in the company and their enthusiasm for investing, which will help the company to expand its financing channels, increase the amount of financing, and reduce the difficulty of corporate borrowing.

The cost of debt financing is the cost that enterprises need to pay for financing from the debt market, which is also regarded as the interest overhead of debt, and the cost of debt financing constitutes a key part of the total cost of financing for enterprises, which has a direct impact on the capital allocation and operational effectiveness of enterprises. Debt financing will have a certain constraint on the enterprise's investment behavior. Financing and investment are two inseparable financial activities in enterprise financial management. In summary, good ESG performance of enterprises can effectively reduce the cost of debt financing, effectively optimize the financial situation and competitiveness of the enterprise, reduce the fundraising overhead, and thus enhance the economic interests of the enterprise, which in turn will bring stronger economic support for the enterprise in the environmental protection industry, and improve the enterprise's capital investment in environmental protection.

Based on this, this paper proposes the following hypothesis H2: Good ESG performance of enterprises helps to reduce the cost of corporate debt financing and thus promote the level of corporate environmental investment.

2.2 Study Design

2.2.1 Samples & Data

This paper selects A-share listed companies from 2008 to 2022 as the sample, excluding companies in financial industry and real estate industry, and excluding companies that are not normally listed, to obtain a total of 32,321 sample observations. The data on firms' ESG performance comes from the ESG rating database of listed companies in Chinese Research Data Services Platform (CNRDS), and all other data comes from China Stock Market & Accounting Research Database (CSMAR).

2.2.2 Model Construction

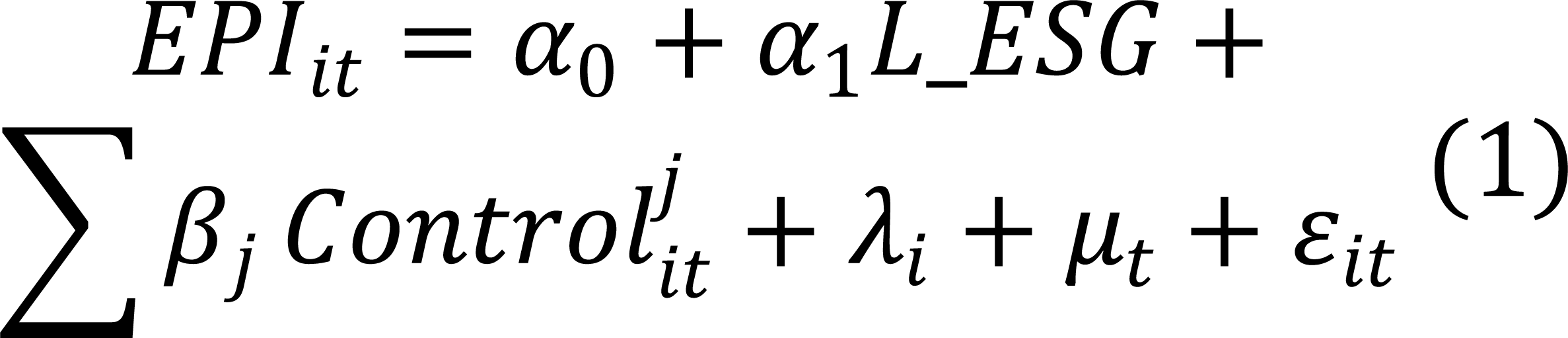

On the basis of the research hypotheses, a fixed effects model is constructed to launch hypothesis testing. In order to test the hypothesis H1 proposed in this paper, the multiple linear regression model Equation (1) is constructed to investigate the impact of corporate ESG performance on environmental investment.

|

Among them, the explanatory variable EPI is the EPI of enterprise i in year t. The explanatory variable L_ESG is the one-period lagged term of firms' ESG scores, and the use of one-period lags helps to mitigate endogeneity problems due to reverse causation, etc. α1 are the regression coefficients of the explanatory variables. λi and μt denote individual fixed effects and time fixed effects, respectively, εit and are residual terms.

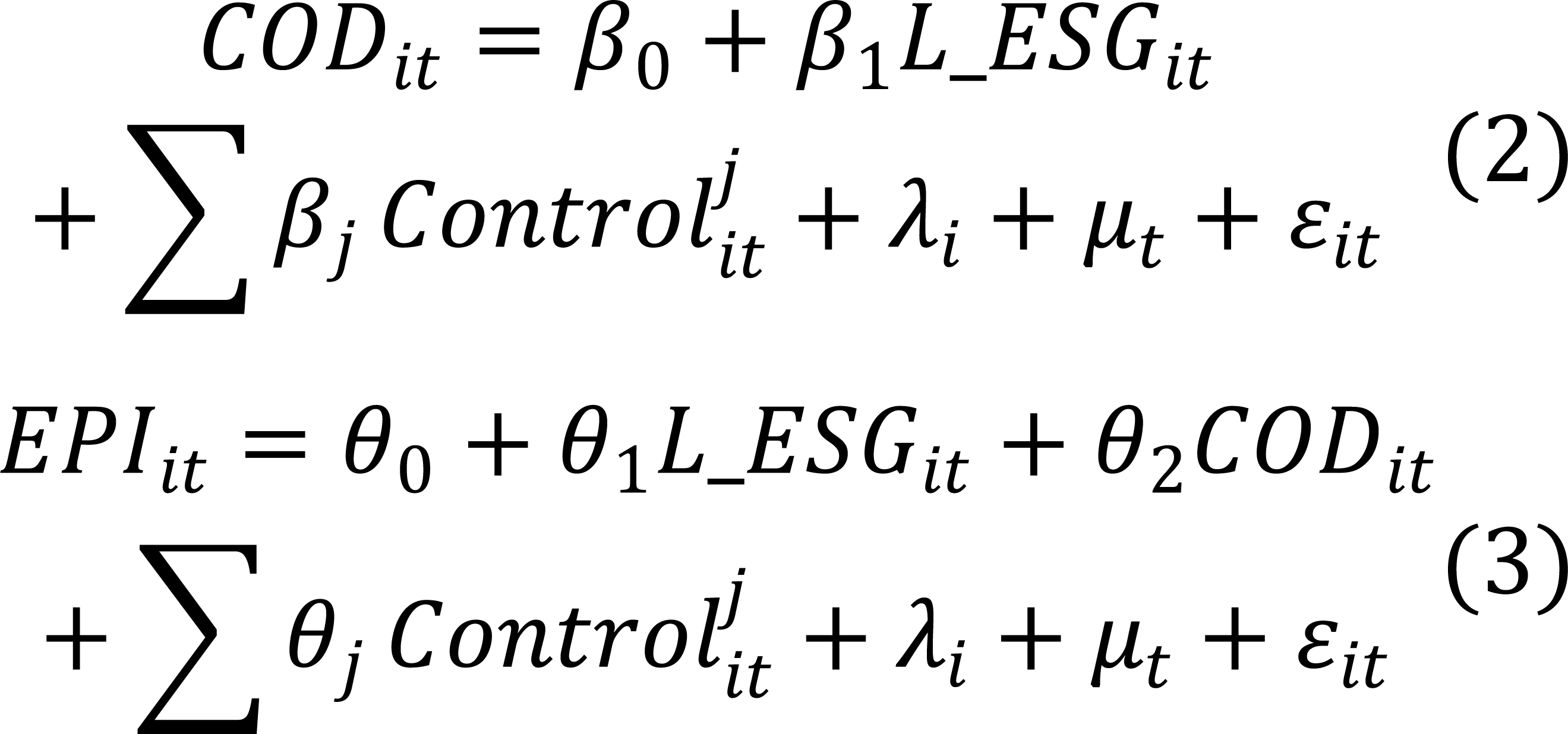

To test hypothesis H2, this paper constructs a mediation effect model, as shown in Equations (2) and (3), to test the mechanism effect of debt financing cost between corporate ESG performance and environmental investment. Where the variable CODit is corporate debt financing cost.

|

2.2.3 Explanation of Variables

The explanatory variables in this paper are the lagged terms of corporate ESG performance. The data on corporate ESG performance comes from the ESG rating database of listed companies in CNRDS. The database is based on international ESG disclosure standards such as ISO 26000, GRI Standards, SASB Standards and the design ideas of well-known ESG databases at home and abroad, and combines with China's ESG disclosure related policies to construct a unique ESG rating system for Chinese companies.

The explanatory variable of this paper is corporate EPI. EPI is the financial investment in environmentally friendly projects, which aims to promote environmental sustainability. Referring to Ma and Gu et al[11,12], this paper filters out the investment expenditure items related to environmental protection from the construction-in-progress in the company's annual report, so as to obtain the amount of corporate EPI, and then takes the ratio of it to the total assets of the company as a measure of the explanatory variable EPI.

Referring to the literature[13], this paper controls for a number of factors that may affect the enterprise's EPI, and the factors include return on total assets (ROA), capital intensity (Density), gearing ratio (LEV), enterprise size (Size), cash level (Cash), and enterprise growth (Growth).

This paper chooses debt financing cost as the mechanism variable. In this paper, the cost of debt financing is measured by using the proportion of finance costs to total corporate liabilities. Where the total liabilities of the enterprise includes long and short-term liabilities, short-term liabilities are composed of short-term borrowings and long-term borrowings due within one year, while long-term liabilities are composed of long-term borrowings, bonds payable, long-term payables and other long-term liabilities. Therefore, the formula for calculating the cost of debt financing in this paper is Cost of Debt Financing (COD)=Finance Charges/(Short-term Liabilities+Long-term Liabilities). Information such as the names and calculations of all variables used in the paper are summarized in Table 1.

Table 1. Definitions of Major Variables

Variable Type |

Name |

Symbol |

Calculation Method |

Explanatory variables |

the EPI of enterprise i in year t |

EPI |

The natural logarithm of corporate environmental investment plus 1 |

Explanatory variables |

Corporate ESG Performance |

L_ESG |

The lag in ESG scores |

Control variables |

Return on total assets |

ROA |

Net Profit/Total Assets |

Capital intensity |

Density |

Fixed Assets/Total Assets at the end of the period |

|

Debt-to-asset ratio |

Lev |

The ratio of total liabilities to total assets at the end of the period |

|

The size of the enterprise |

Size |

The total assets are taken as the natural logarithm |

|

Cash levels |

Cash |

Total monetary funds/assets |

|

Enterprise growth |

Growth |

Growth rate of operating income |

|

Mechanism variables |

Cost of Debt Financing |

COD |

Finance Expenses/(Short-term Liabilities + Long-Term Liabilities) |

3 RESULTS

3.1 Descriptive statistics

The results of the sample descriptive statistics are shown in Table 2. The descriptive statistics cover sample size, mean, standard deviation, median, and minimum and maximum values. The mean of the explanatory variable total EPI is 8.547, the standard deviation is 11.051, the median is 4.467, and the extremes are 0 and 57.561, respectively, with a large difference in the extremes indicating that China's listed companies show significant differences in EPI. The amount of investment in environmental protection of some companies is relatively low, while some others are willing to invest a larger amount of money into the field of environmental protection. The gap reveals the differences in environmental protection awareness and capital investment, and the differences likewise have an impact on the sustainable and healthy development and market power of the companies. The mean ESG performance of the sample firms is 25.569, its standard deviation is 10.733, and the median is 23.457, where the peak reaches 56.914 and the trough is only 4.611.

Table 2. Descriptive Statistics of the Sample

|

Sample Size |

Mean |

Standard Deviation |

Minimum |

Median |

Maximum |

EPI |

32321 |

8.547 |

11.051 |

0.000 |

4.467 |

57.561 |

L_ESG |

32321 |

25.569 |

10.733 |

4.611 |

23.457 |

56.914 |

ROA |

32321 |

0.037 |

0.078 |

-2.834 |

0.038 |

0.786 |

Density |

32321 |

2.380 |

3.413 |

0.072 |

1.851 |

303.339 |

Lev |

32321 |

0.423 |

0.201 |

0.008 |

0.417 |

1.957 |

Size |

32321 |

22.238 |

1.280 |

18.293 |

22.047 |

28.636 |

Cash |

32321 |

0.179 |

0.124 |

0.001 |

0.147 |

0.915 |

Growth |

32321 |

0.434 |

7.025 |

-11.683 |

0.112 |

865.908 |

COD |

28327 |

0.653 |

6.505 |

-423.786 |

1.491 |

99.807 |

3.2 Analysis of Benchmark Regression Results

Table 3 demonstrates the estimation results of model Equation (1), which is a test of the causal relationship between firms' ESG performance and environmental investments. In particular, only time and individual fixed effects are controlled for in column (1); on the basis of column (1), column (2) further incorporates a collection of micro-level control variables; and in column (3), the paper further uses robust standard errors. The empirical results find that the regression coefficients of firms' ESG performance variables (ESG) are positive and pass the statistical significance test, regardless of the adjustments made to the variable settings of the benchmark regression. In column (3), the EPI is positively correlated with the lagged term L_ESG of corporate ESG score at 10% significance level, with a coefficient of 0.02. It indicates that the higher the ESG scores of listed firms, the higher the EPI, which verifies hypothesis H1.

Table 3. The Impact of Corporate ESG Performance on Environmental Investment

|

(1) |

(2) |

(3) |

|

EPI |

EPI |

EPI |

L_ESG |

0.03*** |

0.02** |

0.02* |

|

(2.94) |

(2.46) |

(1.95) |

ROA |

|

0.48 |

0.48 |

|

|

(0.58) |

(0.40) |

Density |

|

0.20*** |

0.20** |

|

|

(10.79) |

(2.48) |

Lev |

|

1.46*** |

1.46 |

|

|

(2.59) |

(1.43) |

Size |

|

1.70*** |

1.70*** |

|

|

(12.65) |

(6.59) |

Cash |

|

-6.03*** |

-6.03*** |

|

|

(-9.63) |

(-7.20) |

Growth |

|

0.00 |

0.00 |

|

|

(0.18) |

(0.18) |

_cons |

10.14*** |

-25.67*** |

-25.67*** |

|

(15.09) |

(-9.09) |

(-4.70) |

Control |

No |

Yes |

Yes |

Individual fixed effects |

Yes |

Yes |

Yes |

Time fixed effect |

Yes |

Yes |

Yes |

Robust |

No |

No |

Yes |

N |

32321 |

32321 |

32321 |

r2 |

0.021 |

0.037 |

0.037 |

F |

14.96*** |

51.68*** |

16.54*** |

Notes: t statistics in parentheses. *p<0.1, **p<0.05, ***p<0.01.

3.3 Analysis of Mechanism Test Results

Table 4 demonstrates the estimation results of models (4.2) and (4.3). The results of the mechanism test show that the estimated coefficient of corporate ESG performance on corporate debt financing cost is significantly negative, indicating that enterprises with higher ESG ratings can obtain lower debt financing cost. At the same time, the cost of debt financing has a more obvious role in promoting corporate environmental investment. After controlling for the variable of debt financing cost, the promotion effect of ESG performance on corporate environmental investment is weakened accordingly, which means that the ESG performance of enterprises can significantly improve the scale of environmental investment by obtaining low-cost debt financing. The cost factor of debt financing becomes particularly important when firms make capital allocation decisions. A firm's unsatisfactory ESG performance may exacerbate financial risks and ultimately increase the cost of debt financing.

Table 4. Transmission Mechanism of Debt Financing Costs in Corporate ESG Performance and EPI

|

(3) |

(2) |

(3) |

|

EPI |

COD |

EPI |

L_ESG |

0.02* |

-0.01** |

0.02 |

|

(1.95) |

(-2.07) |

(1.46) |

COD |

|

|

-0.09** |

|

|

|

(-2.24) |

ROA |

0.48 |

1.80* |

1.07 |

|

(0.40) |

(1.94) |

(0.68) |

Density |

0.20** |

-0.05** |

0.20** |

|

(2.48) |

(-2.10) |

(2.41) |

Lev |

1.46 |

7.26*** |

1.81 |

|

(1.43) |

(10.33) |

(1.60) |

Size |

1.70*** |

-0.20 |

1.64*** |

|

(6.59) |

(-1.46) |

(5.96) |

Cash |

-6.03*** |

-17.87*** |

-7.80*** |

|

(-7.20) |

(-8.25) |

(-7.63) |

Growth |

0.00 |

-0.00 |

0.00 |

|

(0.18) |

(-0.13) |

(0.22) |

_cons |

-25.67*** |

6.29** |

-23.84*** |

|

(-4.70) |

(2.32) |

(-4.11) |

Control |

Yes |

Yes |

Yes |

Individual fixed effects |

Yes |

Yes |

Yes |

Time fixed effect |

Yes |

Yes |

Yes |

Robust |

Yes |

Yes |

Yes |

N |

32321 |

28327 |

28327 |

r2 |

0.037 |

0.142 |

0.037 |

F |

16.54*** |

38.77*** |

14.84*** |

Notes: t statistics in parentheses. *p<0.1, **p<0.05, ***p<0.01.

4 DISCUSSION AND CONCLUSION

This study selected listed companies during the period from 2008 to 2022 as the research object, and adopted the means of empirical analysis to deeply study the impact of corporate ESG performance on their EPI, as well as the mechanism that the cost of debt financing plays a role in it. This study draws the following two conclusions: first, the better the ESG performance of listed companies, the higher the level of corporate environmental investment. The second is that the lower the cost of debt financing, the more significant is the impact of ESG performance on the level of corporate environmental investment. That is, the cost of debt financing is the transmission mechanism between corporate ESG performance and the level of environmental investment. In view of the above two findings, this paper puts forward corresponding policy recommendations.

First, enterprises should assess their performance on ESG in depth and make continuous improvement efforts for themselves based on the ESG management framework. In order to further optimize the effectiveness of ESG, companies should think about how to enhance their corporate governance structure, optimize their corporate governance strategies, raise their environmental awareness, actively take on their social responsibilities, and make efforts to adopt various means of environmental protection. In order to safeguard the transparency and compliance of the company's internal operations, it is necessary to establish a sound corporate governance framework, which includes strengthening the formulation and implementation of strict environmental protection policies, reducing environmental pollution emissions caused by production activities, and improving the efficiency of resource utilization. Establishing a more transparent ESG report and publicizing corporate ESG data and performance in a timely manner enhances mutual trust and reputation. Enterprises should comprehensively incorporate ESG risks into their overall risk management, and strengthen the public transparency and compliance supervision of ESG-related information, so as to reduce possible reputational and legal risks arising from ESG issues.

Secondly, investors should strive to practice ESG investment concepts and give corresponding support to organizations with outstanding ESG performance in their investment and financing activities. Funds provided by investors are actually one of the main financing channels for enterprises and play an indispensable and important role in promoting enterprise development activities. Investors should deeply understand the significance of ESG business performance and actively construct investment portfolios with ESG as the main supporting element. At the same time, they should deeply evaluate the company's performance in EPI and specific operations, and pay close attention to the company's capital allocation to environmentally friendly technologies and sustainability programs. In addition, as a shareholder participant in a company, investors should actively play a role in corporate governance, helping companies to improve ESG standards and transparency of their operations, and establishing communication and cooperation with each company is equally critical. For example, it is important to have in-depth communication with the company's management to understand its ESG strategy and environmental investment plans, and to encourage ongoing reforms, and to encourage merchants who sincerely wish to improve their ESG performance and increase their capital investment in environmental protection to make investment decisions that contribute to change in the industry as a whole. After the project is completed, the investor needs to continuously monitor and evaluate the ESG impact of the investment to ensure that it meets the ESG standards set by the investor, and to adjust its investment direction and strategy based on the company's ESG performance and changes in the cost of debt financing.

Acknowledgements

This work was supported by the University-level Research Project of Guangzhou College of Commerce (Project Number: 2024XJYB011) and the Planning Research Project of The Commerce Economy Association of China (Project Number: 20252226).

Conflicts of Interest

The authors declared no conflict of interest.

Author Contribution

ZHAN Weiling: conceptualization, funding acquisition, supervision and review. YAN Peijin: data curation, formal analysis and Writing - original draft. WANG Xinyi and CAI Huixia: Writing - Review & Editing.

Data Availability

All data generated or analyzed during this study are included in this published article and its supplementary information files.

Copyright and Permissions

Copyright © 2025 The Author(s). Published by Innovation Forever Publishing Group Limited. This open-access article is licensed under a Creative Commons Attribution 4.0 International License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, sharing, adaptation, distribution, and reproduction in any medium, provided the original work is properly cited.

Abbreviation List

EPI, environmental protection investment

CNRDS, Chinese Research Data Services Platform

CSMAR, China Stock Market & Accounting Research Database

References

[1] Alareeni BA, Hamdan A. ESG impact on performance of US S&P 500-listed firms. Corp Gov, 2020; 20: 1409-1428.[DOI]

[2] Kong W. The impact of ESG performance on debt financing costs: Evidence from Chinese family business. Financ Res Lett, 2023; 55: 103949.[DOI]

[3] Tan W, Tsang A, Wang W et al. Corporate Social Responsibility (CSR) Disclosure and the Choice between Bank Debt and Public Debt. Account Horiz, 2020; 34: 151-173.[DOI]

[4] Servaes H, Tamayo A. The Impact of Corporate Social Responsibility on Firm Value: The Role of Customer Awareness. Manag Sci, 2013; 59: 1045-1061.[DOI]

[5] Chang K, Lu N, Li ZS et al. The combined impacts of fiscal and credit policies on green firm’s investment opportunity: Evidences from Chinese firm-level analysis. Manag Decis Econ, 2021; 42: 1822-1835.[DOI]

[6] Ma YB, Lu L, Cui JB et al. Can green credit policy stimulate firms’ green investments? Int Rev Econ Finance, 2024; 91: 123-137.[DOI]

[7] Huang L, Lei Z. How environmental regulation affect corporate green investment: Evidence from China. J Clean Prod, 2021; 279: 123560.[DOI]

[8] Liu G, Yang Z, Zhang F et al. Environmental tax reform and environmental investment: A quasi-natural experiment based on China’s Environmental Protection Tax Law. Energy Econ, 2022; 109: 106000.[DOI]

[9] Porter ME, van der Linde C. Toward a New Conception of the Environment-Competitiveness Relationship. J Econ Perspect, 1995; 9: 97-118.[DOI]

[10] Spence M. Job Market Signaling. Q J Econ, 1973; 87: 355-374.[DOI]

[11] Ma JZ, Huang HY, Zhu Q et al. Corporate Social Responsibility Disclosure, Market Supervision, and Green Investment. Emerg Mark Financ Trade, 2022; 58: 4389-4398.[DOI]

[12] Gu Y, Ho KC, Yan C et al. Public environmental concern, CEO turnover, and green investment: Evidence from a quasi-natural experiment in China. Energy Econ, 2021; 100: 105379.[DOI]

[13] Cui J, Jo H, Na H. Does Corporate Social Responsibility Affect Information Asymmetry? J Bus Ethics, 2018; 148: 549-572.[DOI]